SoFi Could Be One of 2026’s Best Fintech Buys at Current Depressed Levels

The post SoFi Could Be One of 2026’s Best Fintech Buys at Current Depressed Levels appeared first on 24/7 Wall St..

SoFi Technologies (NASDAQ:SOFI) has been one of 2026’s most punished fintechs, with shares down 34.57% year to date even as the underlying business posted record numbers.

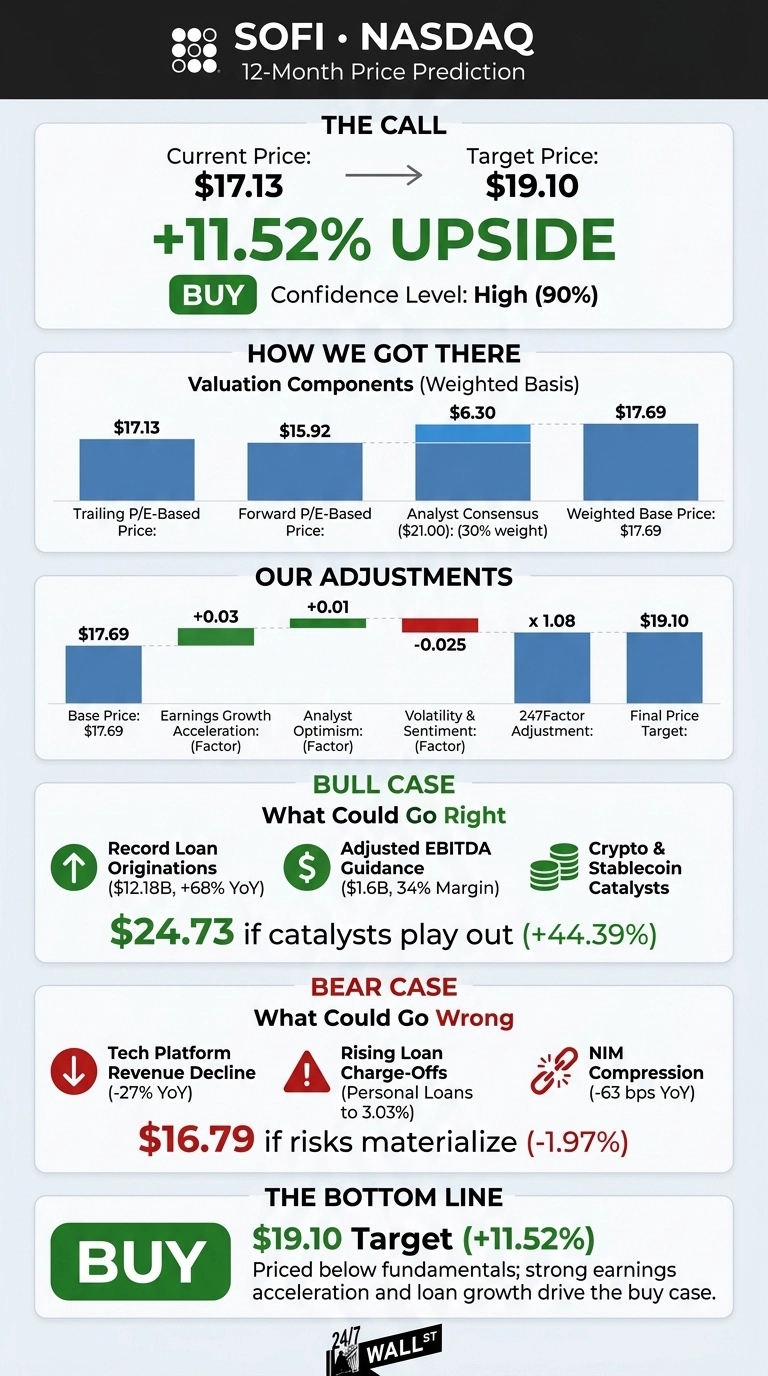

After running the financials through our proprietary model, I think the selloff has overshot the fundamentals. Our 24/7 Wall St. price target for SoFi is $19.10, implying 11.52% upside from the $17.13 close. The recommendation is buy, with high confidence at 90%.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $17.13 |

| 24/7 Wall St. Price Target | $19.10 |

| Upside | 11.52% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $27 to $17: A Brutal First Half for SoFi

SoFi entered 2026 near $26.44 and slid as low as $14.23 on its 52-week low before stabilizing. Shares are up 9.74% over the past month and 21.58% over the past year, but still sit 36% below the $32.73 high. The disconnect with fundamentals is striking.

Q1 2026 revenue of $1.10 billion beat estimates by 4.87%, EPS of $0.12 matched, and GAAP net income jumped 134.45% YoY to $166.73 million. Loan originations hit a record $12.18 billion, up 68% YoY, and deposits reached $40.24 billion.

The Case for $24+

The bull thesis writes itself if you trust management’s guidance. SoFi has guided 2026 adjusted revenue to $4.655 billion (about 30% growth) with adjusted EBITDA near $1.6 billion at a 34% margin, plus a medium-term framework calling for 30%+ revenue CAGR and 38% to 42% adjusted EPS CAGR through 2028.

Catalysts are stacking up: the SoFiUSD stablecoin with Mastercard settlement, crypto trading rollout, Big Business Banking, and a Loan Platform Business that added $3.6 billion in new commitments last quarter.

Anthony Noto said the strategy is “delivering a winning combination of growth and returns”. Our bull case price is $24.73, a 44.39% return, achievable if the multiple rerates on Financial Services revenue growth (currently +41% YoY).

What Could Go Wrong

Bears point to real issues. The Technology Platform segment fell 27% YoY after a large client departure, enabled accounts dropped 16% YoY, and net interest margin compressed by 63 basis points. Credit metrics are softening too, with personal loan charge-offs ticking up to 3.03%.

That said, bulls would argue the Technology Platform weakness reflects one client exit rather than structural decline, and NIM compression is partly the cost of growing low-yield deposits aggressively, which funds over 90% of liabilities.

The Reddit crowd is split, with sentiment swinging from 72 (bullish) in mid-May to 22 (bearish) by month-end. Our bear case lands at $16.79, a modest 1.97% decline.

SoFi Price Prediction 2026-2030

The 24/7 Wall St. price target of $19.10 with a buy rating reflects my view that the YTD selloff has detached price from a fundamentally accelerating business.

The tipping factor is the loan-origination machine running at $12.18 billion per quarter against a stock trading at a forward P/E of 29x. I’d be a buyer here if Q2 2026 confirms 30%+ revenue growth and stable credit metrics. I’d stay on the sidelines if charge-offs jump above 3.5% or the Technology Platform loses another anchor client.

Looking further ahead, here is where our model projects SoFi could trade in coming years, assuming current growth trajectories and credit conditions hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $19.10 |

| 2027 | $21.50 |

| 2028 | $23.00 |

| 2029 | $24.20 |

| 2030 | $25.14 |

These projections assume SoFi executes on its 30%+ revenue CAGR guide. Significant upside could come from stablecoin or crypto monetization, while downside risk centers on credit deterioration or a deeper Technology Platform reset.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and SoFi Technologies didn’t make the cut. Grab the names FREE today.

The post SoFi Could Be One of 2026’s Best Fintech Buys at Current Depressed Levels appeared first on 24/7 Wall St..

추천 콘텐츠

Cancer patient among 100,000 red state voters who lost food aid under Trump's new law

Why Lowe’s Stock Looks Undervalued After Its Q1 Margin Compression Results in 2026

Polis rakam keterangan 7 individu berkait kes 2 askar maut

인기 뉴스

더보기