Is Nebius (NBIS) Stock Worth Buying After Its 16% Five-Day Drop?

TLDR

- Nebius stock jumped 19.5% in June but reversed nearly all of those gains in the first week of July

- Revenue grew 684% year-over-year in Q1 2026, with management targeting over $3 billion for the full year

- A $27 billion deal with Meta Platforms and backing from Nvidia have been key drivers of the rally

- NBIS is up 158% year-to-date but has pulled back 16% over the past five trading sessions, currently trading around $215

- Wall Street has a Moderate Buy consensus with an average price target of $237.38, implying around 10% upside

Nebius Group (NBIS) has been one of the standout performers of 2026. The AI cloud infrastructure company has seen its stock climb 158% year-to-date, more than quadrupling over the past 12 months. But that run has not been smooth, and the latest pullback is a reminder of just how volatile this name can be.

Nebius Group N.V., NBIS

NBIS stock jumped 19.5% in June before giving back nearly all of those gains in the first week of July. As of July 5, the stock is trading around $215.62, down nearly 6% on the day.

The most recent pressure came after Bloomberg reported that Meta Platforms is exploring selling its excess computing capacity. Some investors read that as a potential threat to neoclouds like Nebius. Others pushed back, arguing that demand for AI computing still far outstrips supply.

The irony is not lost on anyone — sellis also one of Nebius’ biggest customers. The two companies have a $27 billion deal in place, with Meta backing around 300 MW of AI capacity. Nvidia’s Jensen Huang has also been active in connecting AI-native companies with Nebius, adding another layer of credibility to the business.

Revenue Growth Has Been Explosive

The numbers behind Nebius are hard to ignore. Revenue was just $105 million in Q2 2025. By Q4, the company had reached an annualized run rate of $1.25 billion. Q1 2026 delivered 684% year-over-year revenue growth.

Management now expects to exceed $3 billion in revenue for 2026, with the pace potentially doubling again in 2027. To support that growth, the company has been aggressively expanding its data center footprint.

Contracted power capacity guidance has jumped from at least 1 GW last August to over 4 GW today. Nebius has already secured 1.2 GW of power and land for a new AI factory in Pennsylvania. It also announced a partnership with Bloom Energy to install additional power for its data center build-out.

Wall Street Is Split

Not everyone is convinced the current valuation holds up. NBIS has reached a market cap of around $55 billion, which is a demanding multiple even when set against its expected 2027 revenues.

Northland analyst Nehal Choksi has a Buy rating with a $248 price target, pointing to Nebius’ shift toward higher-margin, AI-native customers as a reason to stay positive. He sees the Tavily acquisition as a value-add for customers.

Morgan Stanley’s Josh Baer sits on the other side. He has a Hold rating and a $144 price target — well below current levels. Baer acknowledges the customer traction but argues that near-term targets look aggressive, with profitability still unproven and large net new bookings still required to hit guidance.

Wall Street’s overall consensus sits at Moderate Buy, based on six Buy ratings and four Holds. The average price target of $237.38 implies about 10% upside from current levels.

CoreWeave is active in the same space, and any slowdown in AI infrastructure spending could hit NBIS harder than the broader tech sector.

The stock’s 52-week range runs from $43.89 to $299.86, which tells you everything you need to know about the ride investors have been on.

The post Is Nebius (NBIS) Stock Worth Buying After Its 16% Five-Day Drop? appeared first on CoinCentral.

You May Also Like

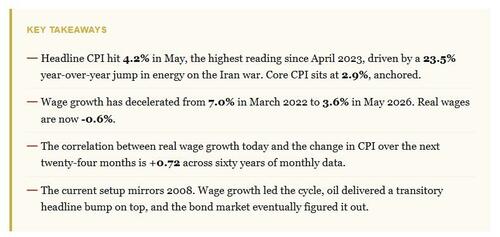

Wage Growth As A Leading Inflation Indicator

Retail Veteran Mitch Gould’s Distribution Platform Addresses Growing Complexity in U.S. Sports Nutrition Market

USA vs Belgium Odds: World Cup 2026 Win Probability and MEXC Prediction Market Guide