Texas Instruments Stock Has Fallen 15% From Its High. Is the Selloff a Bargain or a Warning?

Key Stats for Texas Instruments Stock

- Current Price: $285.43

- Target Price (Mid): ~$520

- Street Target: ~$295

- Potential Total Return: ~80%

- Annualized IRR: ~14% / year

- Earnings Reaction: 19.43% (April 22, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

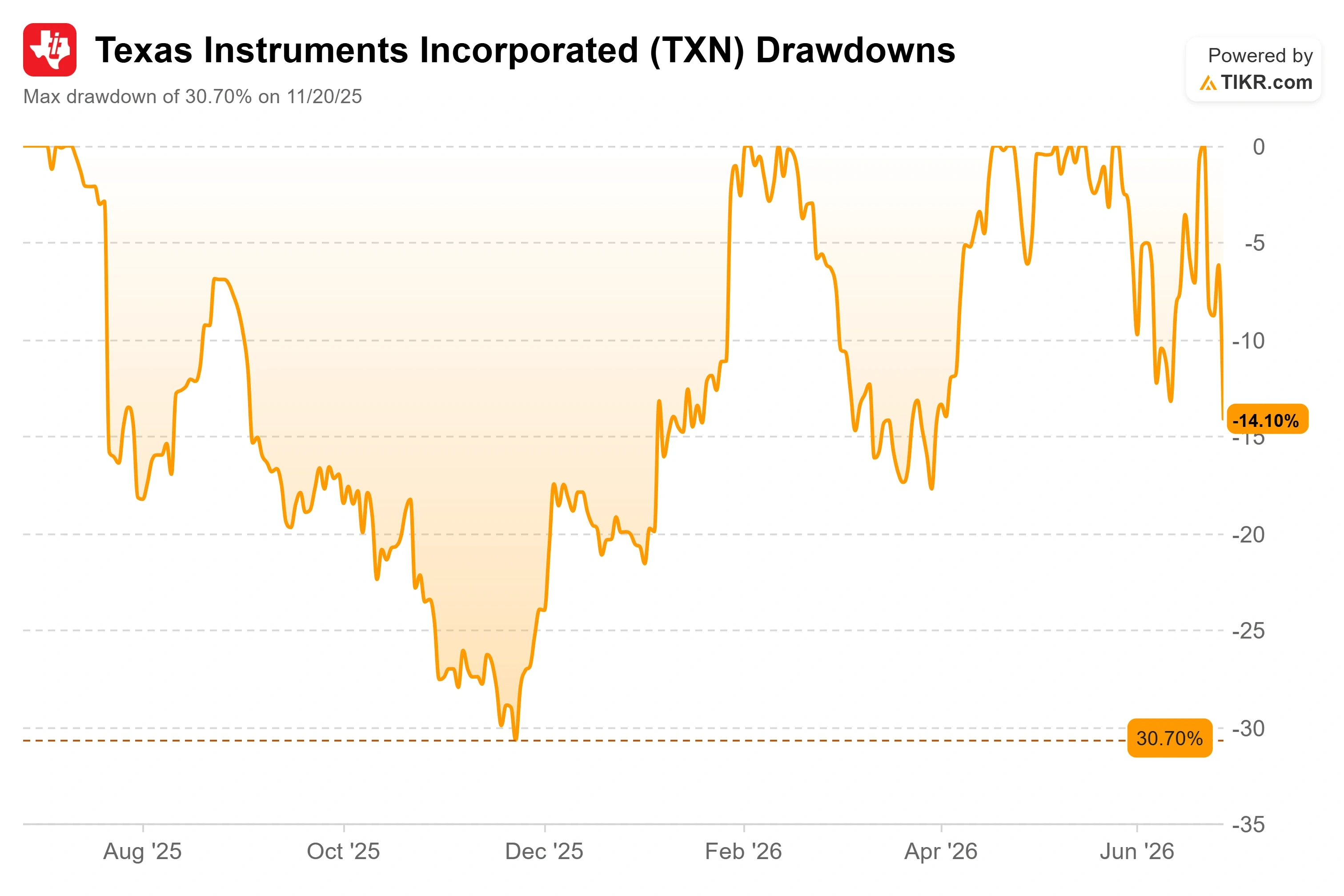

Texas Instruments (TXN) just got punished for something it did not do. The stock closed at $285.43 on June 26, 2026, and it now sits 14.55% below its 52-week high of $334.03. Nothing in the business changed. The damage came from a global chip selloff that started in Asian memory names and rolled through every semiconductor on the tape.

That gap is the whole debate. Texas Instruments stock in 2026 has been a comeback story, up about 75% on the year before the pullback, after a 2025 spent grinding lower. Bulls see a quality analog franchise on sale. Bears see a stock that, even after falling 15%, still trades above where Wall Street thinks it should. The market cannot yet answer the one question that matters: Did June expose a real crack, or did it hand patient investors a discount?

Here is what the selloff actually surfaced, and what the fundamentals say back.

Why the Stock Fell, and Why It Has Nothing to Do With Texas Instruments

The trigger was memory, not analog. A synchronized global semiconductor selloff began overnight in South Korea, where memory makers fell sharply enough to trip circuit breakers, then spread to Wall Street as investors took profits across the AI complex. Texas Instruments makes power and signal-chain chips and has no memory business at all. CEO Haviv Ilan said it plainly at a recent conference: “we don’t build memory anymore.” The stock got swept along anyway because it had run so far, so fast, and a stock that has nearly doubled has the most room to give back.

The damage was severe. The stock fell 8.40% on June 23 to close at $304.36, then kept sliding to finish at $285.43 by June 26. From the $334.03 high, that is a 14.55% drawdown, the sharpest pullback of the stock’s 2026 run.

The drop also followed a wave of bullish analyst action. On June 15, Citi analyst Christopher Danely raised his target to $345 from $280 and reiterated TXN as a top semiconductor pick, citing recent product price increases and TI’s growing share of the data center power market, according to reporting on the Citi call. Shares climbed nearly 7% in the sessions that followed, then gave it all back and more in the selloff.

Texas Instruments Drawdowns (TIKR)

Texas Instruments Drawdowns (TIKR)

See historical and forward estimates for Texas Instruments stock (It’s free!) >>>

The Bear Case the Selloff Put Back on the Table

A sector-driven drop is not a thesis, so the more important question is what the bears are actually arguing now that the stock is cheaper. Three concerns drove the conversation.

The first is that the data center surge was borrowed. TI’s data center revenue grew about 90% year-over-year in the first quarter, and skeptics argue a chunk of that was pull-forward demand, orders that landed at TI only because rival analog chipmakers hit foundry bottlenecks. If competitors clear their capacity constraints in the back half of 2026, the worry is that TI gives some of those temporary share gains back.

The second is margin pressure from the factory bet. TI is finishing a six-year capacity buildout that Ilan sized at “more than $20 billion,” and that spending shows up as depreciation. TIKR’s own estimates show depreciation and amortization rising from about $1.9 billion in 2025 to roughly $2.3 billion in 2026, a step-up of nearly $370 million that weighs on gross margins if revenue growth slows. Pair that with a dividend payout that consumes most of current earnings, a 94.1% payout ratio per TIKR, and the bears argue there is little cushion if the cycle stalls.

The third is insider selling into a leadership change. On June 2, TI named Julie Knecht as its next CFO, effective August 1, 2026, succeeding Rafael Lizardi, who is retiring after 25 years. SEC Form 4 filings show Lizardi exercised stock options and sold the acquired shares in the months before the transition, at prices around $307 to $309. That is a routine exercise-and-sell pattern rather than an outright dump, and he still held more than 119,000 shares directly and indirectly afterward, but it added to the unease while the stock was already falling.

What Management Said Before the Selloff, in Its Own Words

Here is where the timing helps the bull side. Four weeks before the drop, CEO Haviv Ilan addressed the two biggest bear points directly at the Bernstein Strategic Decisions Conference on May 28, 2026, and his answers are more specific than anything the post-selloff coverage produced.

On the “borrowed demand” worry, Ilan did not lean on the AI narrative. He pointed to the industrial recovery, historically TI’s largest market, as the real engine. Industrial fell almost 50% from its peak during the downturn and grew close to 35% year-over-year in the first quarter, yet Ilan noted it still sat “15% below peak,” meaning the recovery has room left rather than being late-cycle. He also flagged the return of factory automation and robotics orders that customers had delayed during tariff anxiety, calling it “my biggest excitement.”

On data center durability, Ilan sized the opportunity rather than hyping it. He pegged TI’s data center addressable market at roughly $7.5 billion last year, growing about 65%, with TI capturing about $1.5 billion, or a 20% share. Then he described TI’s outperformance: “I called the TAM at about 65% growth. So far, 1 quarter, we grew 90%.” That gap between market growth and TI’s growth is the share gain the bulls are paying for, and Ilan put the content opportunity “in the tens of thousands of dollars per rack.” It matters because it reframes the data center from a fragile spike into a structural content story across power, signal chain, and cooling.

On the factory bet that worries the bears, Ilan was blunt about the payoff: “free cash flow should grow as CapEx goes down and demand goes up.” That is the entire investment case in one sentence, and the model is where it gets tested.

Texas Instruments Free Cash Flow & Margins (TIKR)

Texas Instruments Free Cash Flow & Margins (TIKR)

See how Texas Instruments performs against its peers in TIKR (It’s free!) >>>

Where the Premium Sits Versus Peers

The valuation is the crux. Even after falling 15%, TXN trades at an NTM EV/EBITDA (next-twelve-months enterprise value to core earnings) of 23.21x. Among large semiconductor peers, it sits below Advanced Micro Devices at 51.36x and Marvell at 46.69x, but well above Broadcom at 18.68x and Taiwan Semiconductor at 14.24x. On forward P/E, TXN’s 34.58x runs above Broadcom’s 23.18x and Qualcomm’s 19.27x.

Is the premium justified? It is defensible only if both the data center shares gains and the industrial recovery holds. TI earns a higher multiple than Broadcom or TSMC because of its margin profile and its 100% free cash flow return model, but for a company whose 10-year revenue CAGR (compound annual growth rate) is just 3.1%, the market is paying for an acceleration that has only recently shown up in the numbers. If either engine slips, a stock trading above the Street’s average target has the most room to fall, which is exactly what June previewed.

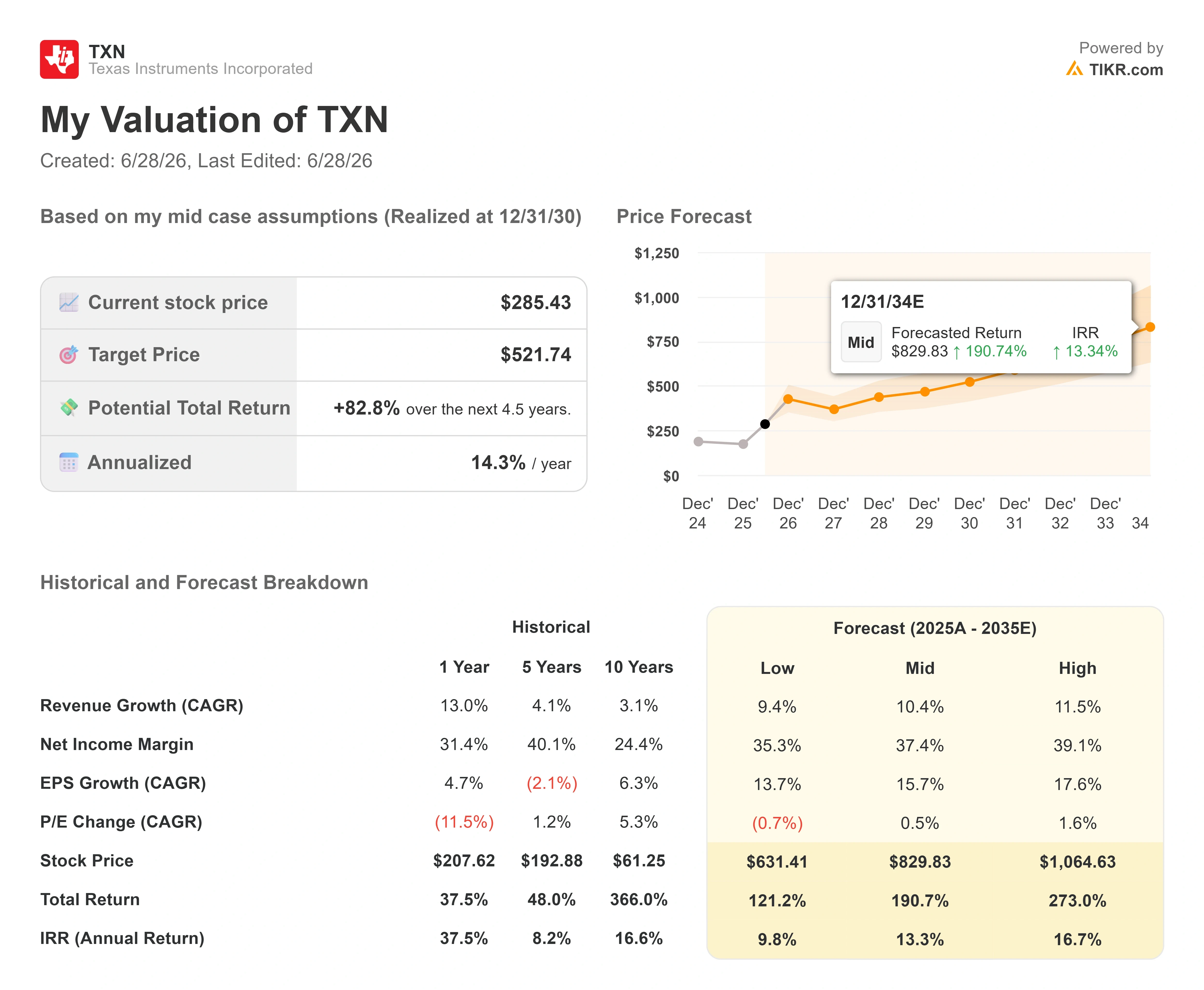

TIKR Advanced Model Analysis

- Current Price: $285.43

- Target Price (Mid): ~$520

- Potential Total Return: ~80%

- Annualized IRR: ~14% / year

Texas Instruments Advanced Valuation Model (TIKR)

Texas Instruments Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Texas Instruments stock (It’s free!) >>>

This analysis uses the TIKR mid-case, realized at the end of 2030. The mid-case target is around $520, implying a potential total return of around 80% over roughly 4.5 years, or about 14% annualized. That sits far above the Street’s average target of around $295, which lands just above where the stock trades today, meaning consensus sees little upside from here while the model sees a wide gap.

Two revenue drivers carry the model. The first is the data center ramp, where TI is growing well above a market expanding at around 65%. The second is the industrial recovery, still about 15% below its prior peak and only one or two quarters into its rebound. The margin driver is factory utilization: as internal 300mm wafer production absorbs fixed costs, the model assumes net income margins expand toward around 37% in the mid-case from about 31% recently. The primary risk is the demand durability question, that data center pull-forward fades and industrial stalls before utilization catches up to the spending.

The upside: if both end markets hold and free cash flow inflects as management guides, the mid-case around $520 is reachable, and the current price looks like a discount.

The downside: if the recovery proves shallow, depreciation and a high payout leave little cushion, and a stock above the Street’s target corrects further.

Conclusion

The thesis gets its first hard test on July 22, 2026, when Texas Instruments reports second-quarter results. Watch data center growth above everything else. Holding near the first quarter’s roughly 90% year-over-year pace confirms the share-gain story and tells you June was a window. A slowdown toward the market’s 65% rate is the first real crack, and after the year’s run, that is when a stock trading above the Street’s target has the most to lose.

Watch industrial too: a second straight quarter of broad sequential growth turns a hopeful recovery into a confirmed one. Good looks like both are holding. Bad looks like either slipping. The tape sold the stock on fear in June. The numbers in late July will say whether the fear was right.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Texas Instruments?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Texas Instruments, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Texas Instruments alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Texas Instruments on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

XRP Ledger sees a remarkable 71.7% surge in activity! What does this mean for the price?

America's unmet promise — and most shameful secret

Wirex and Ultra Stellar Launch Native Stellar Payment Infrastructure to Power Millions of Users and AI Agents