Arista Networks Stock Is Up 55% Over the Past Year. Here’s What Investors Should Know

Key Stats for ANET Stock

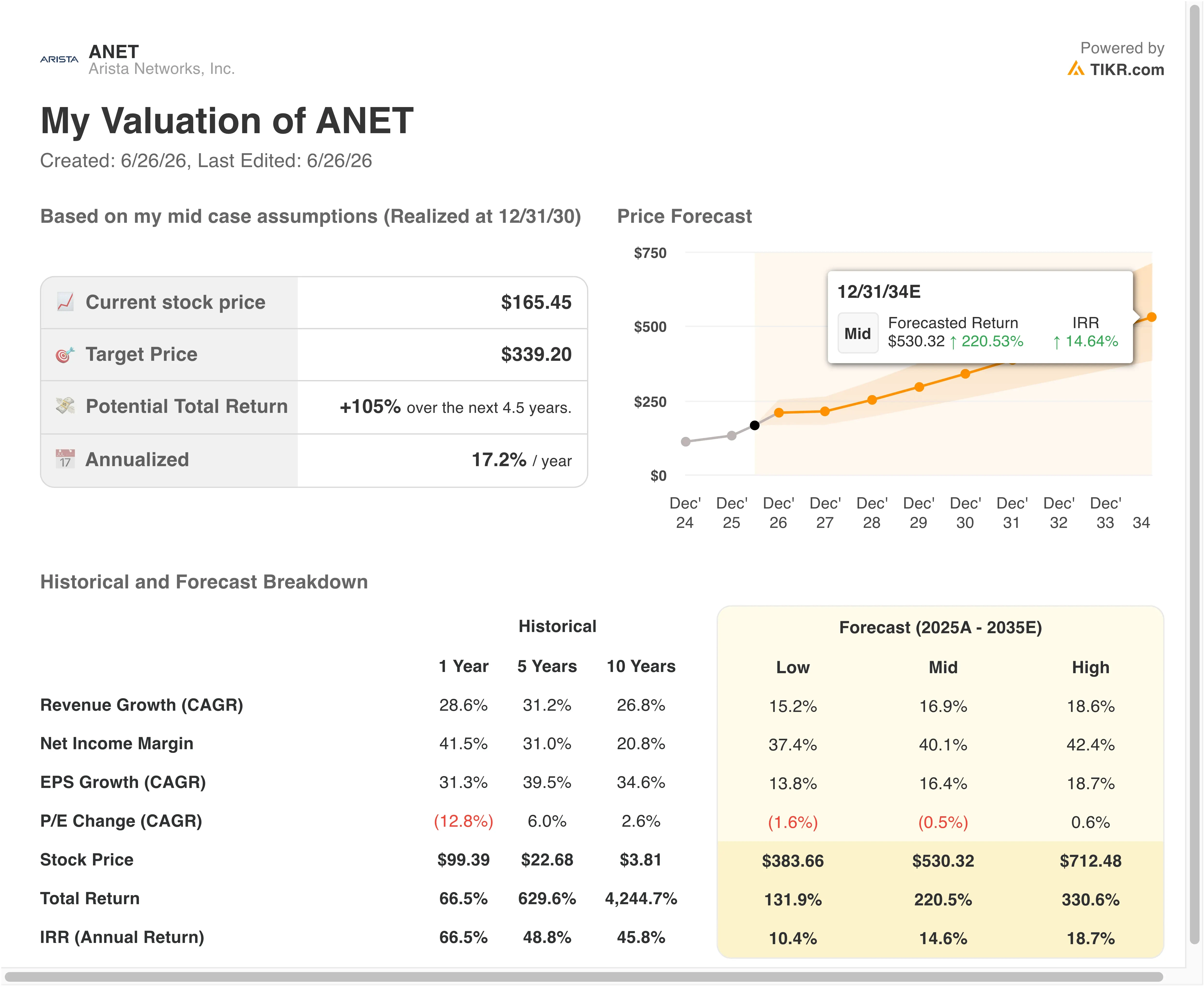

- Past week’s performance: -9.7%

- 52-week range: $97 to $180

- Valuation model target price: $262

- Implied upside: +58.3% over the next 2.5 years

See Arista Networks’ full analyst estimates and valuation model on TIKR (It’s free) >>>

ANET Stock Insiders Are Selling. The AI Networking Story Hasn’t Changed.

Arista Networks (ANET) saw its president and CTO Kenneth Duda dispose of $5.12 million in shares on June 25. That sale was the latest in a sustained pattern of insider selling that has been running through late May and June. Ten percent owner Andreas Bechtolsheim, one of Arista’s co-founders and one of the most significant individual stakeholders in the company, executed multiple block sales totaling over $100 million across May and June. CEO and Chair Jayshree Ullal also sold $2.13 million in shares on May 29.

Insider selling on this scale naturally prompts questions. But it is important to distinguish between insider selling that reflects concern about business fundamentals and insider selling that reflects portfolio management by long-term holders with enormous unrealized gains. Arista stock has risen over 70% in the past 12 months.

Bechtolsheim’s stake in Arista has been one of the most valuable equity positions in Silicon Valley for over a decade, and systematic selling at elevated prices is standard wealth management practice for institutional insiders at this level.

ANET Basic EPS (TIKR)

ANET Basic EPS (TIKR)

Arista’s business fundamentals have not changed. Q4 fiscal 2025 results, reported in February, showed adjusted EPS of $0.82 against an $0.76 estimate. Arista presented at the Bank of America Global Technology Conference in June and the William Blair Growth Stock Conference in June, where management reiterated the company’s confidence in AI networking demand from hyperscale customers.

Going forward, the question ANET investors are really asking is whether the AI networking buildout, which has driven Arista’s extraordinary growth, has more duration than the market currently prices in. If ANET stock sustains its level through Q2 results, expected July 30, management’s commentary on AI cluster orders will be the key input.

See analysts’ growth forecasts and price targets for ANET (It’s free) >>>

Is Arista Stock Still Attractive After a 55% Run?

ANET Guided Valuation Model (TIKR)

ANET Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 24.3%

- Operating Margins: 47.4%

- Exit P/E Multiple: 39.1x

Based on these inputs, the model estimates a target price of $262, implying 58.3% total upside from the current share price and a 20% annualized return over the next 2.5 years.

A 20% annualized return after a 72% one-year run is a result that surprises many investors who assume the stock has gotten ahead of itself. The reason the model still generates that return is straightforward: Arista’s earnings are growing fast enough that even at today’s elevated share price, the forward multiple is not as stretched as the absolute price suggests.

ANET Guided Valuation Model (TIKR)

Arista’s LTM operating margin of 42.8% is already exceptional, and the model projects a slight improvement to 47.4% by the end of 2028. That incremental margin expansion reflects operating leverage as revenue grows faster than headcount and R&D spend. Arista’s NTM P/E of roughly 44x sits below the 39.1x exit multiple assumption in the model, which implies the model is actually embedding very modest multiple compression rather than expansion.

The 24.3% revenue CAGR assumption aligns with Arista’s LTM revenue growth of 28.6% and the forward two-year consensus CAGR of 26.2%. The model is not forecasting acceleration, but rather a modest deceleration consistent with a larger revenue base. That conservatism gives the model credibility because it does not require heroic assumptions to generate a 20% annualized return.

Compare Arista’s valuation against its own history and peers using TIKR’s model tools >>>

Arista vs. Cisco and Juniper in AI Networking

Arista’s most direct competitors in the data center networking market are Cisco Systems (CSCO) and Juniper Networks (JNPR), though the competitive dynamic between them has shifted significantly over the past three years.

Cisco is the incumbent in enterprise networking, with a dominant market share across traditional campus and branch office switching. But in the high-speed data center and AI cluster networking market, Arista has been consistently taking share.

Cisco’s revenue growth has been far more modest than Arista’s, and its operating margins, while healthy, reflect a much higher cost structure tied to a global sales force and traditional product lines. Cisco trades at roughly 17x to 18x forward earnings, a massive discount to Arista’s 41x, which reflects both slower growth and a heavier exposure to the legacy enterprise market.

ANET NTM P/E vs CSCO and JNPR (TIKR)

ANET NTM P/E vs CSCO and JNPR (TIKR)

Juniper Networks was acquired by Hewlett Packard Enterprise in a deal completed in 2024, making HPE the combined entity’s owner. That integration has been complex, and the combined business lacks the pure AI networking focus that Arista has built systematically over the past decade. Arista’s ROIC of 30.8% and ROE of 31.5% both significantly exceed what Cisco reports, which shows that Arista is deploying its capital far more efficiently, even at premium valuations.

The insider selling wave does not change this competitive picture. Arista’s product advantage in spine-leaf data center architecture and its early moves into AI Ethernet Consortium-standard networking for large AI clusters position it well ahead of Cisco in the highest-growth segment of the networking market.

See what analysts expect from Arista’s Q1 earnings after a yearly rally >>>

What’s Driving ANET Stock Going Forward?

The AI cluster networking opportunity is the single most important forward driver for Arista. As hyperscale operators like Microsoft, Google, Meta, and Amazon continue to build out dedicated AI training clusters, those clusters require extremely high-bandwidth, low-latency network fabrics connecting thousands of GPUs. Arista’s 400G and 800G switches are purpose-built for exactly this environment, and the company has been explicit that these AI-related deployments are a growing proportion of total orders.

The Ethernet versus InfiniBand question is a recurring topic in AI networking discussions. InfiniBand, a competing interconnect technology owned by Nvidia, has traditionally been preferred for the most demanding AI training workloads because of its lower latency.

But a consortium of major tech companies, including Microsoft and Meta, has been pushing for Ultra Ethernet as an open standard alternative. Arista is a founding member of the Ultra Ethernet Consortium, which positions it well if Ethernet-based AI networking gains further traction against InfiniBand.

Arista’s Q2 2026 results are expected on July 30. Orders from hyperscale customers during Q2 will determine whether the revenue growth trajectory holds near the high-20% range or decelerates. Any commentary from management about multi-year AI networking commitments from cloud customers would be a significant positive catalyst.

The insider selling, while large in absolute dollar terms, is a secondary consideration relative to the business trajectory. Andreas Bechtolsheim has been selling Arista shares for years while the stock has continued to climb. The pattern reflects systematic diversification by a founder with an enormous concentrated position, not a change in conviction about where Arista is headed.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Arista Networks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ANET, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ANET alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze ANET stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

What Happens to the XRP Price if the Crypto Bear Market Gets Worse?

Solana SOL Reclaims $72, But Fading On-Chain Metrics Signal Weakening DEX Momentum

Bitcoin Price Prediction: Analysts Believe BTC Bottom Window Is Open