Can Credo Hit $300 By Year-End?

The post Can Credo Hit $300 By Year-End? appeared first on 24/7 Wall St..

Credo Technology (NASDAQ:CRDO) has become one of the AI infrastructure trade’s most explosive winners, with shares up 252.99% over the past year and 80.28% year-to-date.

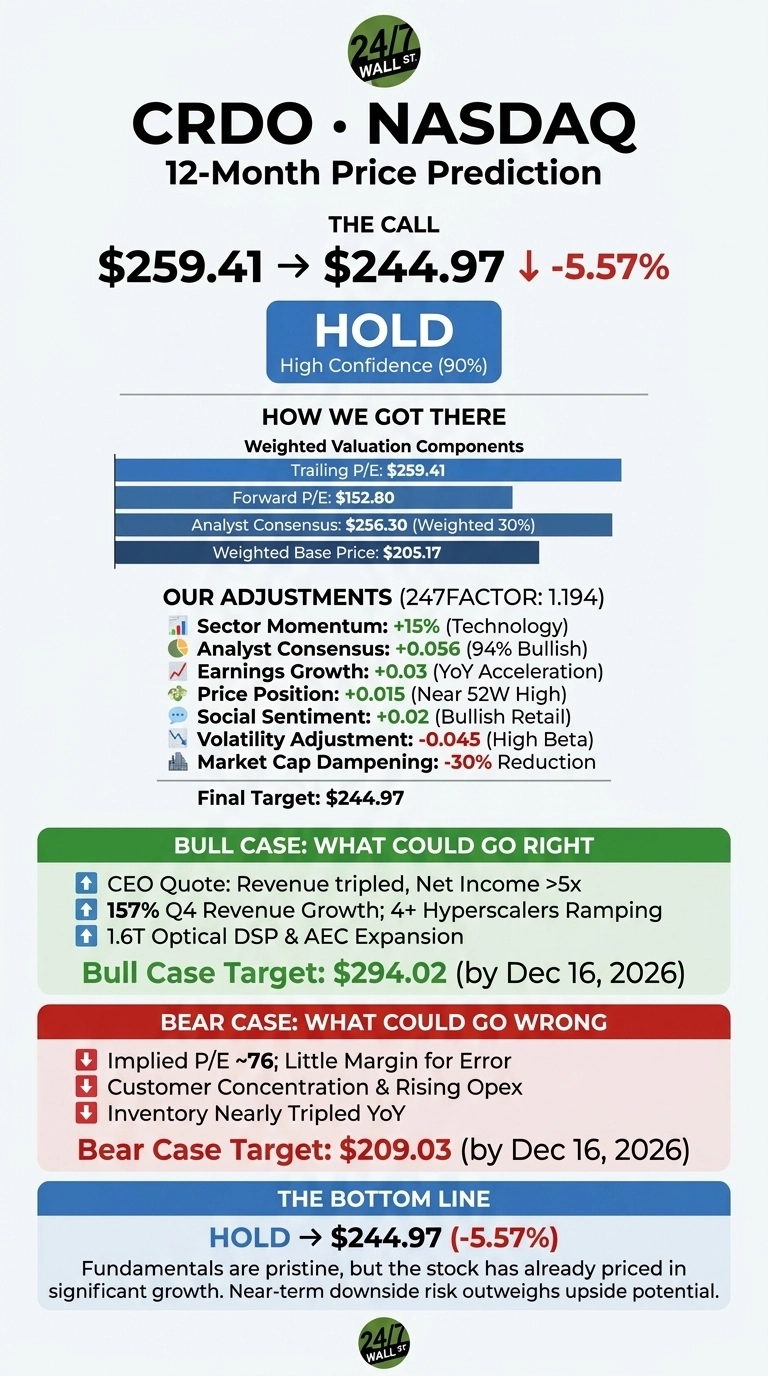

The question on every shareholder’s mind is whether the stock can punch through $300 before December. Our 24/7 Wall St. price target for Credo is $244.97, sitting just below the current quote of $259.41. We rate shares a hold with high conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $259.41 |

| 24/7 Wall St. Price Target | $244.97 |

| Upside/Downside | -5.57% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target of $244.97 sits modestly below where Credo trades today. This is one of the AI complex’s most volatile names, and real upside could come from a hyperscaler raising AI capex guidance or from Credo’s 1.6T optical DSP reaching production faster than expected. Consider our target one datapoint among many. The full bull case below outlines why CRDO could still outrun our model.

From $79 to $259 in a Year

Credo has rallied 16.71% in the past week and 50.67% in the past month, putting shares roughly 5% off the 52-week high of $270.21.

The fuel was Q4 FY2026 earnings reported June 1, 2026: revenue of $437 million grew 157% YoY, and non-GAAP EPS of $1.16 beat the $1.03 estimate. Full fiscal 2026 revenue more than tripled to $1.34 billion with non-GAAP net income jumping more than 5x to $662 million. Q1 FY2027 guidance calls for revenue of $465M to $475M.

The Case for $300+

Bulls argue Credo is still early. CEO Bill Brennan told investors that fiscal 2026 saw revenue more than triple and net income rise 5x, adding that Credo enables customers to accelerate cluster time-to-stability, maximize GPU utilization, improve network reliability, and reduce overall infrastructure power and operating costs.

A fourth hyperscaler is ramping past the 10% revenue threshold and a fifth is qualifying. Active Electrical Cables run 1,000 times more reliable at half the power of optical, opening node-to-tor and scale-up markets that could be an order of magnitude larger than scale-out. Our bull-case trajectory has CRDO reaching $294.02 by December 16, 2026 and crossing $302.23 by March 2027.

The Risks Worth Watching

Credo trades at an implied P/E near 76 on forward EPS, leaving little margin for an AI capex digestion phase. Customer concentration remains real, though bulls counter that the top-three mix is diversifying as new hyperscalers ramp.

Inventory nearly tripled YoY and operating expenses are rising, but management frames the R&D buildout as funding optical projects and forthcoming business pillars. Our bear case sees CRDO at $209.03 by year-end if AI orders pause.

24/7 Wall St.

24/7 Wall St.

Credo Price Prediction 2026-2030

I land on hold with 90% confidence and a 24/7 Wall St. price target of $244.97. The fundamentals are pristine, but the stock has already done the work.

I’d be a buyer if shares pulled back to the low $200s or if Credo guides Q2 FY2027 above $500M. I’d stay on the sidelines if the implied P/E pushes past 90 without a corresponding guide raise. Hitting $300 by year-end is achievable in a bull tape, but the base case says it slips into early 2027.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $254.73 |

| 2027 | $278 |

| 2028 | $305 |

| 2029 | $335 |

| 2030 | $365 |

These projections assume Credo continues executing on hyperscaler ramps and optical expansion. Significant upside or downside could result from a step-change in AI capex or a shift toward in-house silicon at major cloud customers.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Credo Technology Group didn’t make the cut. Grab the names FREE today.

The post Can Credo Hit $300 By Year-End? appeared first on 24/7 Wall St..

You May Also Like

This red state might attempt to alienate its Democratic voters

Bitcoin Exchange Binance Announces New Listings on its Futures Platform! Here Are the Details

US ADP Employment Change 4-Week Average Dips to 25.5K, Signaling Cooling Labor Market