Alphabet Stock Price Prediction: The Forecast Points to 20% Upside

The post Alphabet Stock Price Prediction: The Forecast Points to 20% Upside appeared first on 24/7 Wall St..

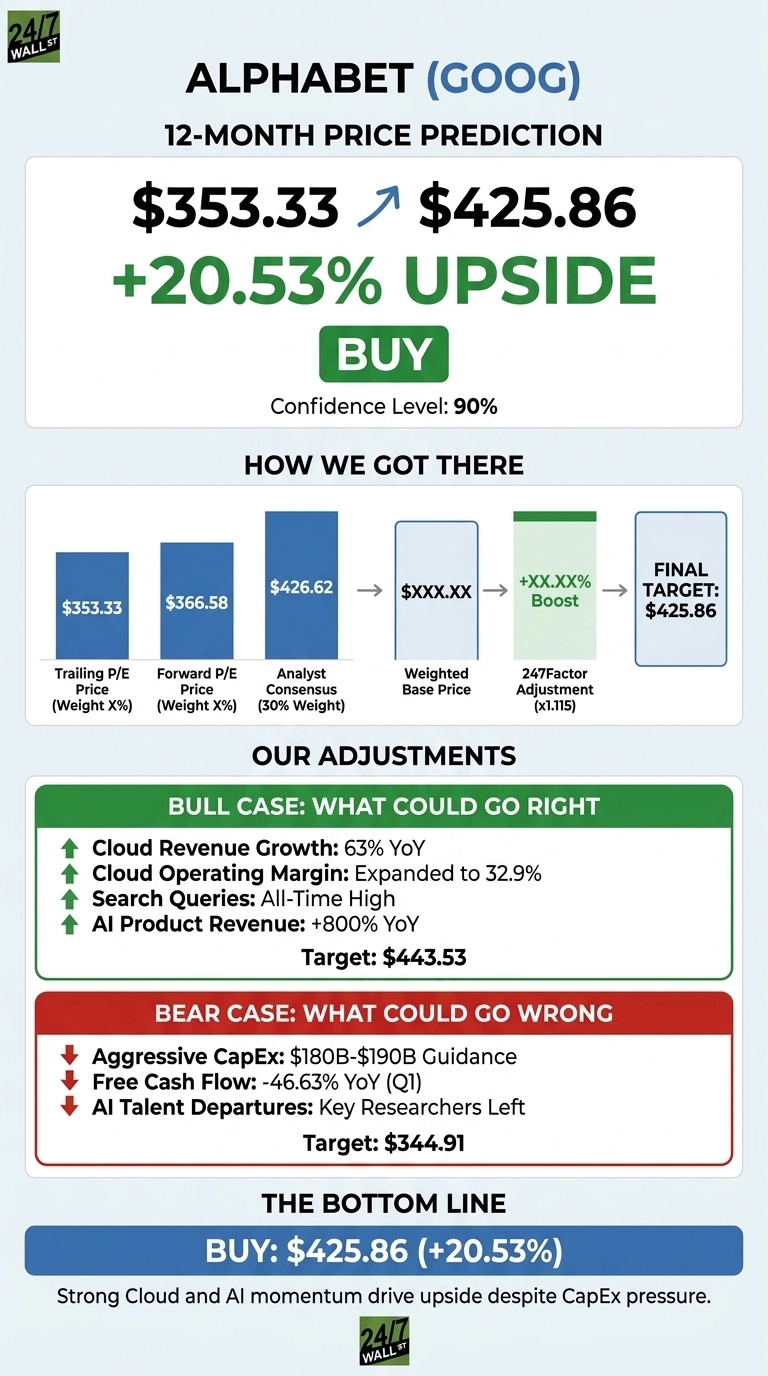

Alphabet (NASDAQ:GOOG) is one of the cleanest bull setups in mega-cap tech right now. Cloud is compounding at 63%, operating margins are expanding, and management just committed to nearly doubling AI infrastructure spend. The stock trades at $353.33 after a 6.08% pullback over the past month, and I see that dip as an entry point.

Our 24/7 Wall St. price target for Alphabet is $425.86, implying 20.53% upside over the next 12 months. My recommendation is buy, with 90% confidence.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $353.33 |

| 24/7 Wall St. Price Target | $425.86 |

| Upside | 20.53% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Blowout Quarter, Then a June Pullback

Alphabet has nearly doubled in a year, up 99.75% over 12 months and 12.74% year to date. The stock now sits 6% below its 52-week high of $404.23 after a June cooling.

The Q1 2026 report on April 29, 2026 was the catalyst. Revenue hit $109.90 billion, up 21.8% year over year, and EPS came in at $5.11 versus a $2.63 consensus.

Google Cloud grew 63% to $20.03 billion, with backlog nearly doubling quarter over quarter to $462 billion. Recent retail sentiment took a hit on news of two top AI researchers departing to OpenAI and Anthropic, but the stock has stabilized.

Why Bulls See a Breakout Ahead

The bull thesis rests on three pillars. First, cloud momentum is undeniable. Cloud operating margin expanded from 17.8% to 32.9% year over year, and revenue from products built on Gemini grew nearly 800% year over year.

Second, search is thriving. Query volume is at an all-time high, with Search revenue up 19%. Third, the ecosystem monetizes. Paid subscriptions hit 350 million, and Waymo now runs over 500,000 autonomous rides weekly.

The Street backs this up. GOOG carries 14 Strong Buy and 44 Buy ratings against zero Sells. If cloud continues to compound at 60%+ and AI monetization inflects in search, a bull case toward $443 becomes readily defensible.

The Risks Worth Watching

The bear case starts with capital intensity. Alphabet raised 2026 CapEx guidance to $180 billion to $190 billion, and CFO Anat Ashkenazi said “We expect our 2027 CapEx to significantly increase compared to 2026.” Q1 free cash flow already fell 46.63% year over year.

Bulls counter that this reflects deliberate investment against unprecedented internal and external demand for AI compute resources, not deteriorating unit economics.

Other watch items: a $3.5 billion European Commission fine in Q3 2025, competitive pressure from OpenAI and Anthropic, and Q1 net income padded by $36.91 billion in unrealized equity gains that will not recur. A bearish scenario points to $344.91, roughly flat from here.

Alphabet Price Prediction 2026-2030

My 24/7 Wall St. price target of $425.86 is a buy with 90% confidence. The tipping factor is Google Cloud’s $462 billion backlog, which locks in growth visibility that no other Alphabet segment has offered before.

I’d be a buyer here if you believe cloud can sustain 40%+ growth into 2027. I’d stay sidelined if you think 2026 CapEx of $190 billion permanently caps free cash flow generation. On balance, the risk/reward favors owning it.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $425.86 |

| 2027 | $478 |

| 2028 | $535 |

| 2029 | $580 |

| 2030 | $624 |

These projections assume Alphabet continues executing on cloud, search, and AI monetization. Significant upside or downside could result from Waymo commercialization, regulatory action, or shifts in AI competitive positioning.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Google didn’t make the cut. Grab the names FREE today.

The post Alphabet Stock Price Prediction: The Forecast Points to 20% Upside appeared first on 24/7 Wall St..

You May Also Like

BetOnline Take The Prize Easter Promotion Offers $30k in Cash Prizes!

Trump’s “ Extremely Hard” Hits Hard On Bitcoin, But Some Altcoins Make It Through