Intel Stock Rose 6% to a 25-Year High. Here’s What the Stock Could Do

Key Stats for Intel Stock

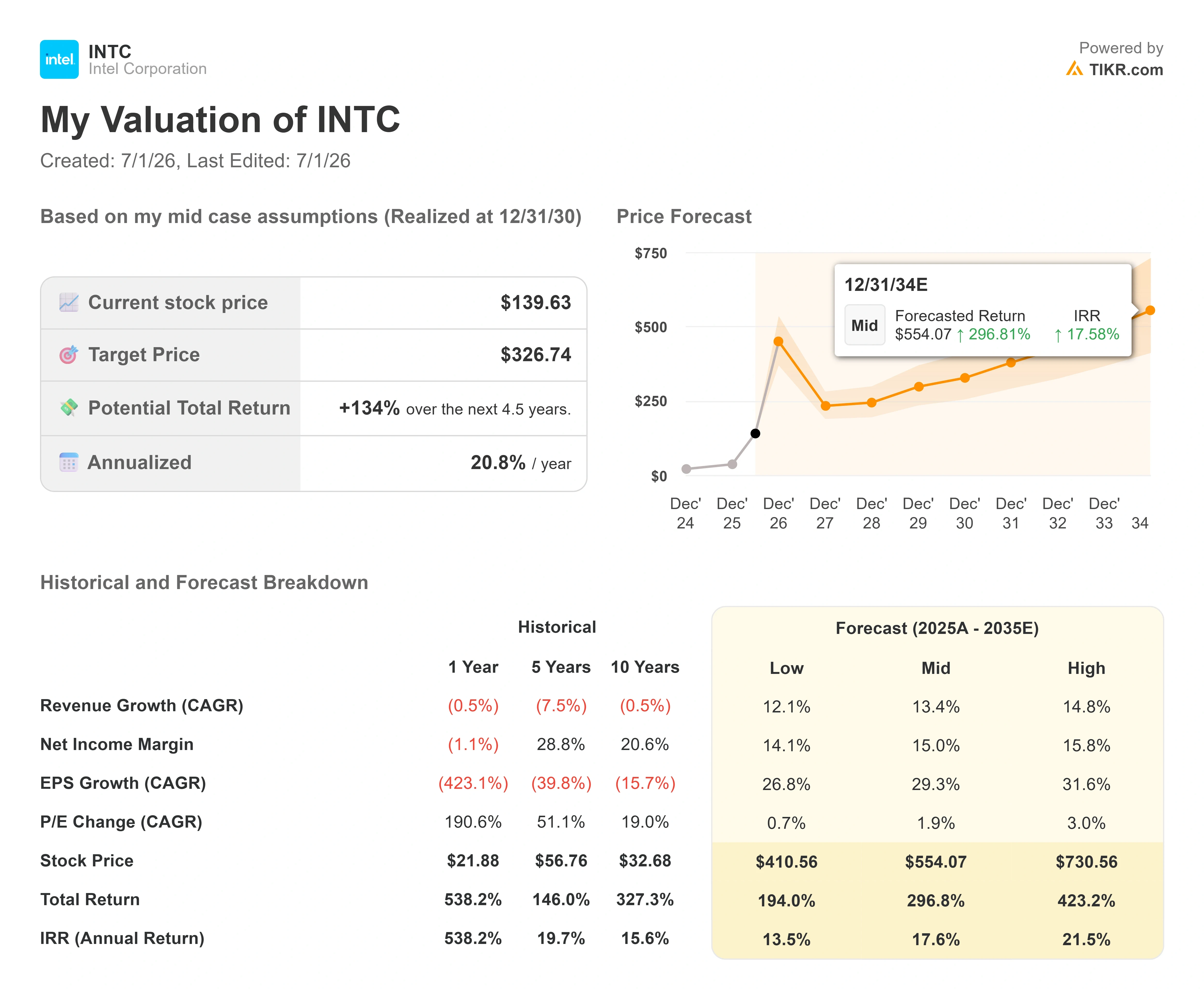

- Current Price: $139.63

- Target Price (Mid): ~$327

- Street Target: ~$99

- Potential Total Return: ~134%

- Annualized IRR: ~21% / year

- Earnings Reaction: 23.60% (April 24, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Intel Corporation (INTC) closed up 6.01% at $139.63 on June 30, its highest level in roughly 25 years, and for once the move had less to do with a headline than with a factory. For most of 2026, Intel has traded on politics and promises: a rumored Apple deal, a claimed government stake, a stacked deck of partnership announcements. That made the rally easy to dismiss as a stock story. What changed in the back half of June is that the story started producing receipts.

The receipt that matters most arrived on June 16. At the 2026 VLSI Symposium, Intel Foundry confirmed that 18A-P, the first performance upgrade to its 18A manufacturing process, had entered risk production, which is the low-volume pilot stage right before high-volume manufacturing. According to Intel’s own newsroom release, the node hit the timeline management first, giving customers a year earlier, and it delivers 9% higher performance at the same power. For a company that spent years synonymous with delays, an on-schedule node is the headline, not a footnote.

That milestone reframes the entire debate. The bulls and bears here are no longer arguing about whether Intel is a turnaround. They are arguing about pace and price. The stock is up more than 250% in 2026, it trades near a 25-year high, and Wall Street’s mean target still sits at around $99, roughly 29% below the current price. That gap is the tension. Either the Street is badly behind a business that is inflecting, or the market has already paid for a recovery that has not shown up in reported profits yet. The question the market cannot yet answer is simple: Is on-time execution enough to justify a price that the analysts covering the stock still will not endorse?

Why the Execution Story Suddenly Has Teeth

The reason execution matters more than any single deal is that Intel’s margins live and die on factory yields. When yields improve, more revenue drops through a cost base that is largely fixed. When they slip, the whole model stalls. So the most important thing management said recently was not about Apple. It was about the timeline for those yields, and it came from the CFO.

Speaking at the Bank of America 2026 Global Technology Conference on June 2, Intel CFO David Zinsner walked investors through the roadmap in Intel’s investor relations materials and said the company’s goal of reaching the yields that generate strong margins had been an end-of-2027 target, then added a correction that investors have been chewing on since. “Based on the progress we’ve made to date now, we are likely going to pull in those milestones by at least a quarter, potentially even a little more,” Zinsner said. That matters because Intel’s margins hinge on yields, so pulling the yield milestones forward pulls forward the point at which the fixed-cost fab base starts working for the company instead of against it. It is worth being precise about scope: Zinsner said the yield milestones are pulling in, but he kept Intel Foundry’s own breakeven target at exiting 2027, noting the only thing that would delay it is being “more wildly successful” and spending on new capacity. On TIKR’s estimates, LTM free cash flow is still negative, so the pace of that margin recovery is the swing factor in the whole thesis.

Zinsner also confirmed Intel is steering the business toward what he called the “Rule of 45,” meaning revenue growth plus operating margin summing to 45. He framed it as a multi-year, aspirational goal, not a next-year promise. But it tells you what the company is solving for: profitable growth, not growth at any cost. That is a different Intel than the one that spent a decade compounding revenue at low single digits.

The detail most investors have overlooked sits one node further out. Zinsner said Intel’s next-generation 14A process is already ahead of where 18A was at the same stage of maturity. “When you look at kind of yield and performance measures at this point in time and maturity of 14A compared to that same moment in time for 18A, we’re ahead,” he said. He described 14A as a more standard, industry-conventional design that should be a “rinse and repeat” of the hard lessons learned on 18A. If that holds, it means the painful part of Intel’s process transition may be behind it, not ahead.

Intel Free Cash Flow & Margins (TIKR)

Intel Free Cash Flow & Margins (TIKR)

See historical and forward estimates for Intel stock (It’s free!) >>>

The Catalyst Stack Behind the June Surge

The June move was not one event. It was a cluster. 18A-P risk production landed on June 16. Two days later, on June 18, shares jumped after President Trump said Apple had agreed to design and build chips with Intel in the United States, though neither company formally confirmed the terms. Bank of America had already double-upgraded the stock from Underperform to Buy earlier in June with a $135 target, then raised that target to $160 on June 25 on a larger 2030 chip market. Then on June 30, the day of the 6% close, Cantor Fitzgerald analyst C.J. Muse raised his target to $150 from $90, citing the AI infrastructure buildout, while keeping a Neutral rating.

Read together, those four events explain the re-rating. Read carefully, they also explain the risk. The Apple partnership still has no disclosed volume, dollar figure, or timeline, and 18A-P has only just entered risk production, which means any Apple chip volume is realistically a 2027 event or later. The market is paying today for commitments that mostly have not been signed. That is the bear case in one sentence, and it is why the Street’s target still trails the tape.

Where the Valuation Actually Sits

Intel is not cheap on any conventional screen, and pretending otherwise would be dishonest. The stock trades at around 36x NTM EV/EBITDA against a peer group median closer to 19x, and its NTM price-to-earnings multiple is far into triple digits because earnings are only now recovering off a depressed base. Put Intel next to its most-cited peers on revenue, and the picture is more nuanced. On NTM enterprise value to revenue, Intel sits at around 12x, roughly in line with NVIDIA at around 11x and Broadcom at around 13x, and well above Micron at around 6x. The market is not valuing Intel like a broken chipmaker anymore. It is valuing it like a credible foundry and AI-infrastructure play, which is exactly what the re-rating bulls wanted and bears distrust.

Whether that premium is justified comes down to one variable: does the margin recovery Zinsner described actually land? If 18A and 14A yields keep climbing and factory utilization rises, the fixed-cost base turns from an anchor into a tailwind, and today’s rich EV/EBITDA multiple compresses fast as earnings catch up. If yields stall or foundry losses persist, the stock is priced for a recovery that arrives late, and the 29% gap to the Street’s target closes the wrong way. The whole investment case sits on that fork.

Intel NTM EV/EBITDA (TIKR)

Intel NTM EV/EBITDA (TIKR)

See how Intel performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $139.63

- Target Price (Mid): ~$327

- Potential Total Return: ~134%

- Annualized IRR: ~21% / year

Intel Advanced Valuation Model (TIKR)

Intel Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Intel stock (It’s free!) >>>

Using TIKR’s mid-case scenario, the model points to a target price of around $327 by the end of 2030, implying around 134% total return from the current price, or roughly 21% annualized over about 4.5 years. This is the mid case, chosen because it reflects a credible execution path rather than either a collapse or a best-case blowout, and because it lines up with the yield-improvement cadence management has actually guided to.

The two revenue growth drivers are Data Center and AI, where server CPU demand is running ahead of supply as AI workloads shift from training toward inference and agentic computing, and Intel Foundry, where external customer commitments on 18A and 14A begin converting into wafer revenue. The margin driver is factory utilization: as advanced-node yields rise and volumes fill Intel’s fixed-cost fabs, gross margin expands. The primary risk is a yield or timing slip on 18A-P and 14A that pushes the margin inflection out past 2027 and keeps foundry losses on the books longer than the market has priced.

The upside case is that on-time 18A-P execution proves the roadmap is real, 14A ramps cleanly, and Intel re-rates as the default American foundry with margins to match. The downside case is that the Apple and Terafab commitments stay unsigned, yields disappoint, and a stock trading near a 25-year high gives back the premium it built on promises.

Conclusion

The next real test is Q2 2026 earnings on July 23. Watch non-GAAP gross margin against the roughly 39% level Intel guided to for the quarter. Hold at or above that mark, and the yield-and-pricing story Zinsner described is working, and the “pull in by at least a quarter” comment starts to look conservative. Slip meaningfully below it, and the margin-recovery timeline shifts right, which is the one thing a stock priced this richly cannot absorb. The other thing to watch on that call is whether any of the June partnership headlines finally arrive as signed volume commitments. Until they do, Intel remains a stock where the execution is now real, but the price still assumes the rest of the story shows up on schedule.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Intel?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intel, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intel alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Intel on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Hamster Kombat Daily Cipher 2 July 2026: Play And Win

Lime (LIME) Goes Public: Scooter Company’s $167M IPO Sees Overwhelming Investor Demand