Meta Stock Price Prediction: The Forecast Sees a Path to $800+

The post Meta Stock Price Prediction: The Forecast Sees a Path to $800+ appeared first on 24/7 Wall St..

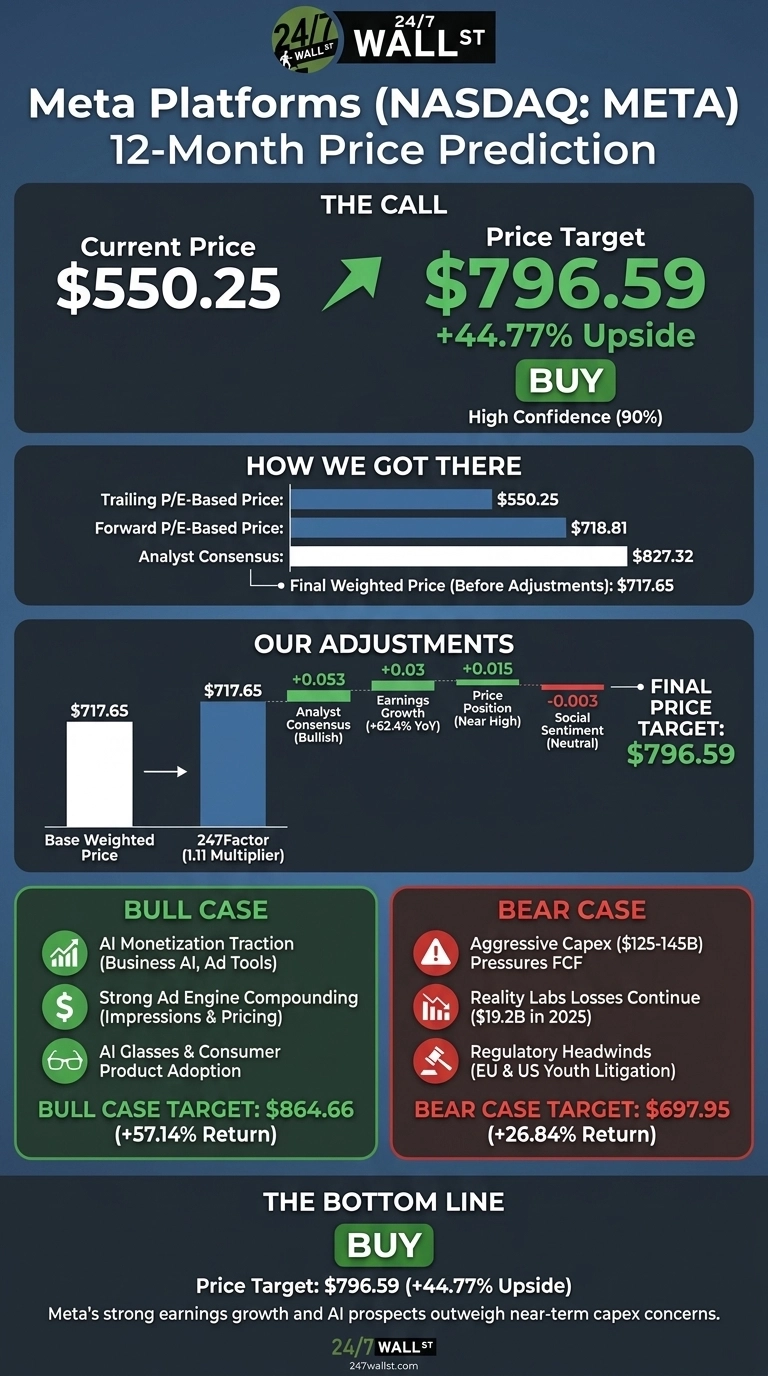

Meta Platforms (NASDAQ:META) has had a rough first half of 2026, but our model sees a compelling risk-reward setup in mega-cap tech. With shares down 16.5% year to date and the AI capex narrative dividing investors, the pullback has gone too far.

Our 24/7 Wall St. price target for Meta is $796.59, implying 44.77% upside over the next 12 months. Our model’s rating is buy, with a confidence level of 90%, which we consider high.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $550.25 |

| 24/7 Wall St. Price Target | $796.59 |

| Upside | 44.77% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $785 Peak to $550 Pullback

Meta topped near $785 in August 2025 before drifting lower for ten months to down 13.3% over the past month and down 23.97% over the past year. The stock trades just 4% off its 52-week high of $793.65 on a calendar basis but well below recent peaks, with the 200-day moving average sitting at $650.02.

Q1 2026 fundamentals tell a different story. Revenue delivered revenue of $56.31 billion, up 33.08% YoY, with EPS of $10.44 versus a $6.66 consensus, a 56.79% beat. Underlying EPS was roughly $7.31.

Ad impressions rose 19% while average price per ad climbed 12%. Management raised 2026 capex guidance to $125 billion to $145 billion, fueling the “incinerating capital” narrative that gathered momentum in late June.

Why Bulls See a Breakout Ahead

The bull case rests on Meta’s ad engine compounding while AI investment turns into monetizable products. Q1 saw Business AI weekly conversations rise to 10 million from 1 million at the start of 2026, the Value Optimization Suite cross a $20 billion annual run rate, and AI glasses daily active users triple year over year.

Zuckerberg framed the strategy bluntly: “We are on track to deliver personal superintelligence to billions of people.” Wall Street agrees, with 8 strong buys, 49 buys, and zero sell ratings. Our bull-case scenario points to $864.66 over 12 months, a 57.14% return.

The Risks Worth Watching

The bear case starts with capex. The $125 to $145 billion 2026 capex nearly doubles 2025 spending and pressures free cash flow, which fell 19.39% in 2025. Reality Labs lost $19.2 billion last year, and youth-related litigation trials in 2026 could be material. Polymarket traders assign only 0.5% probability to META hitting $700+ in June to near-term success.

Bulls counter that the forward P/E of 17 is undemanding, and capex feeds the Muse Spark model and custom silicon platform built with Broadcom that powers over 1 gigawatt of compute. Our bear scenario still produces $697.95, a 26.84% gain.

The Setup at Current Levels

The 24/7 Wall St. price target of $796.59 reflects a confident buy rating. Meta trades at a forward P/E of 17 and PEG of 0.795 while compounding revenue at 33% with industry-leading margins.

The bull thesis rests on whether ad pricing power and engagement gains can fund the AI buildout without margin collapse. The bear case strengthens if capex spirals past $150 billion in 2027 with no monetization payoff. The risk-reward at $550 favors buyers.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $796.59 |

| 2027 | $816.11 |

| 2028 | $1,049.06 |

| 2029 | $1,219.81 |

| 2030 | $1,384.57 |

These projections assume Meta converts AI capex into monetizable products at its current pace. Significant upside or downside could result from agentic commerce traction, AI glasses adoption, or regulatory shocks from EU and US youth litigation.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Meta didn’t make the cut. Grab the names FREE today.

The post Meta Stock Price Prediction: The Forecast Sees a Path to $800+ appeared first on 24/7 Wall St..

You May Also Like

68% of global BTC miners came from the U.S., Russia, and China, Q1 2026

Ethereum Institutional launched to boost Wall Street adoption after foundation layoffs