Mastercard Stock Holds 29 Buy Ratings Despite Middle East Travel Hit

Key Takeaways for Mastercard Stock as of July 2026

- 29 analysts rate Mastercard stock a buy, with 9 additional outperforms against just 2 holds and zero sells, one of the most lopsided splits the stock has carried in the past year, and a mean target of $644 implies 23% upside from the $522 close.

- TIKR’s mid-case model puts Mastercard stock at $948 by December 2030, an 82% total return, or 14% annualized over 4.5 years.

- Trading well below that Street mean despite beating on every reported line in Q1, Mastercard stock looks undervalued against the EBITDA growth the market is underpricing.

- CFO Sachin Mehra flagged a Q2 revenue guide at the low end of low double digits on the July 1 call, with Middle East conflict pulling cross-border travel growth down from 8% to 2% inside four weeks.

Mastercard stock just cleared 29 buy ratings and a $644 mean target, yet Q2 guidance already prices in a war headwind. See where TIKR’s model lands on MA for free →

What Mastercard’s Q1 Beat Hides a Cross-Border Travel Slowdown

MA Stock Q1 2026 Earnings in USD (TIKR)

MA Stock Q1 2026 Earnings in USD (TIKR)

Mastercard (MA) posted $8.40 billion in Q1 2026 revenue, beating the Street’s $8.26 billion estimate by 2% and growing 16% year over year. EBITDA came in at $5.41 billion, a 77 basis point margin beat against consensus, and adjusted EPS reached $4.60 against a $4.41 estimate. Net income climbed 20% year over year to $4.10 billion.

That strength came almost entirely from value-added services, not the core card network. CEO Michael Miebach told investors on the Q1 earnings call that VAS revenue grew 18% on a currency-neutral basis with zero contribution from acquisitions, since the business had already lapped its Recorded Future purchase. CFO Sachin Mehra confirmed the growth was organic, comparing it against 22% VAS growth in Q4 that had carried a 3 point acquisition boost.

Beneath the headline beat, cross-border travel told a different story. Worldwide cross-border volume grew 13% in Q1, but Mehra broke out the deceleration: growth fell from 8% in Q1 to just 2% in the first four weeks of April, driven by the Middle East conflict, portfolio migration timing, and the shift of Ramadan and Easter into different quarters. Mastercard estimates roughly 6% of its cross-border volume touches the GCC and Israel combined, counting both issuing and acquiring exposure.

Miebach used the moment to lean into two structural bets instead. Mastercard is deepening its Agent Pay partnership with OpenAI and confirmed nearly all Mastercard-branded cards worldwide are now enabled for agentic payments.

And the company’s planned acquisition of BVNK, a stablecoin infrastructure platform, is expected to close within the next couple of months, adding a basis-points-on-volume revenue model to a business TIKR data shows accelerating on the EBITDA line even as travel volumes soften.

Mastercard just confirmed nearly every card worldwide is now agentic-payment ready, even as cross-border travel growth fell from 8% to 2%. Track the shift on TIKR for free →

Wall Street Still Sees 23% Upside in Mastercard Stock Despite the Guide

Street Analysts Target for MA Stock (TIKR)

Street Analysts Target for MA Stock (TIKR)

29 of the analysts covering Mastercard stock rate it a buy, with 9 additional outperform ratings against just 2 holds, 2 with no rated opinion, and zero sells, one of the most lopsided splits the stock has carried in the past year. The mean target sits at $644, implying 23% upside from the $522 close on July 1, 2026.

That target has held roughly flat since March 2026 even as the stock corrected from a $571 close in December, suggesting the Street’s model isn’t yet fully absorbing the Q2 guidance cut Mehra flagged on the July 1 call.

Wall Street Expects Mastercard Stock’s EBITDA to Grow 13% Through Fiscal 2027

MA Stock EBITDA Trajectory (TIKR)

MA Stock EBITDA Trajectory (TIKR)

Mastercard’s EBITDA reached $5.41 billion in the quarter ending March 2026, up 18% year over year, before the Street’s forward estimates step down.

Analysts model EBITDA growth of 12% for the June 2026 quarter, then 13% for the September quarter and nearly 15% for the December quarter, a sequential acceleration that assumes the Middle East disruption fades as Mehra’s base case predicts.

Accrodingly, that trajectory rests on VAS continuing to outrun the core network, the same dynamic that carried Q1. But the Street’s 12% estimate for the June quarter sits below what Mastercard delivered in Q1, before accounting for any conflict resolution Mehra’s guidance assumes. If the war ends on schedule and cross-border travel recovers as projected, the September and December estimates may prove conservative rather than aggressive.

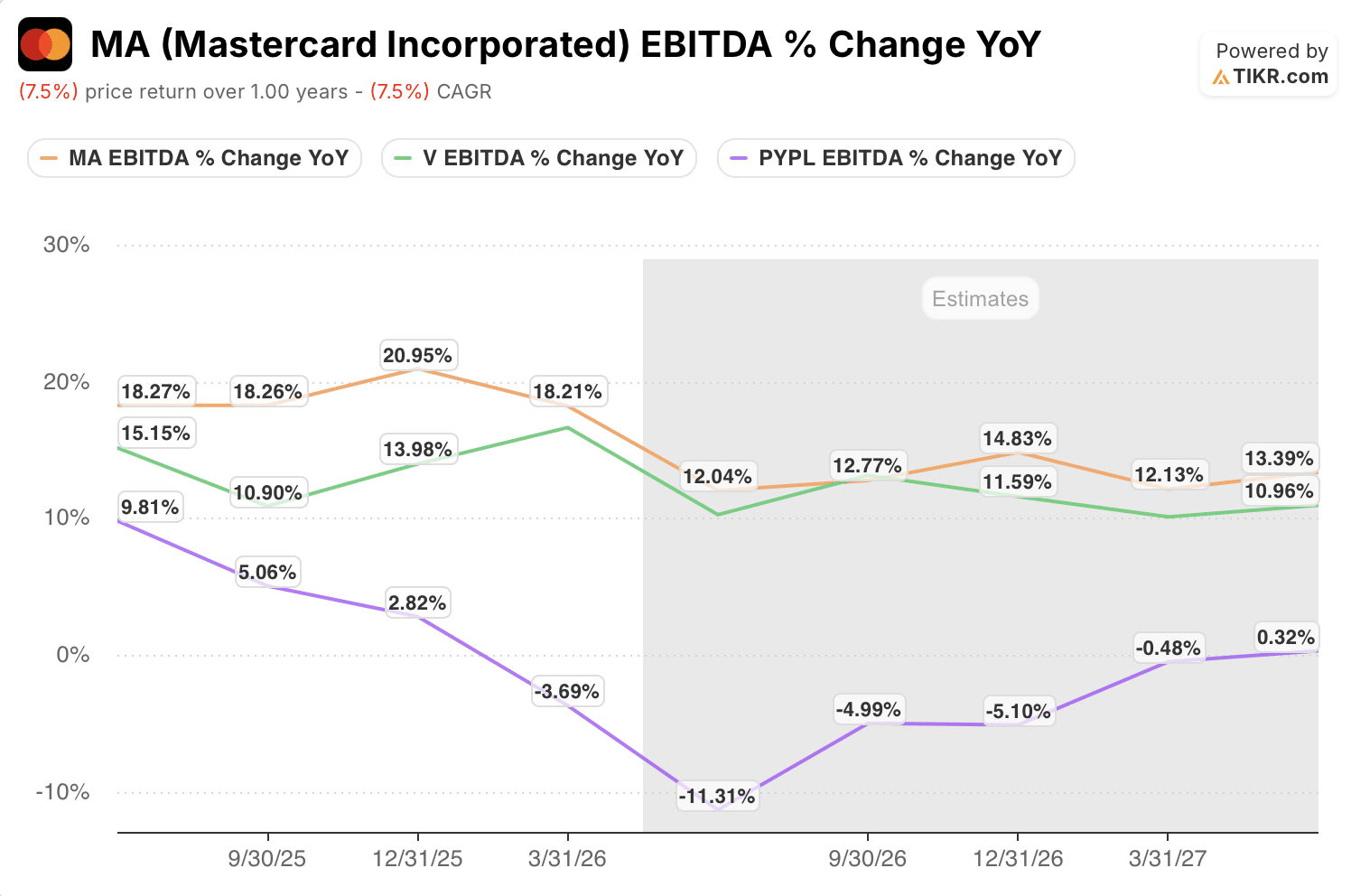

Mastercard Stock Holds the EBITDA Growth Lead Over Visa and PayPal Through 2027

MA Stock EBITDA Growth vs Peers (TIKR)

MA Stock EBITDA Growth vs Peers (TIKR)

Mastercard’s EBITDA grew 18% year over year in the quarter ending March 2026, topping Visa’s (V) 11-14% band and far outpacing PayPal (PYPL), whose growth fell from 10% to negative 4% across the same stretch.

Forward estimates show Mastercard and Visa converging into a 12-15% range through 2027, while PayPal troughs at negative 11% in June 2026 before clawing back to roughly flat by March 2027.

Mastercard enters the forecast window with the highest EBITDA growth of the three and holds that edge even as the gap to Visa narrows.

TIKR’s $948 Target on Mastercard Stock Holds if Agentic and Stablecoin Bets Scale on Schedule

TIKR’s mid-case model values Mastercard at $948 by December 2030, implying 82% total return from the current price of $522, or 14% annualized over 4.5 years.

MA Stock Valuation Model Results (TIKR)

MA Stock Valuation Model Results (TIKR)

That return profile sits ahead of the 7% annualized return Mastercard delivered over the past 5 years, positioning the stock’s forward case as a re-acceleration rather than a continuation of recent history.

The case rests on EBITDA margins holding near 64%, a level Mastercard has sustained through Q1 2026 despite the cross-border headwind, while VAS keeps compounding at double-digit rates independent of travel volumes.

If BVNK closes on schedule and Agent Pay volume scales the way nearly universal card enablement suggests it can, the 9% mid-case revenue CAGR embedded in TIKR’s model has room to prove conservative.

TIKR’s model puts Mastercard stock at $948 by 2030, a 14% annualized return case built before the BVNK stablecoin deal even closes. Check the full model on TIKR for free →

Should You Invest in Mastercard Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Mastercard Incorporated stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Mastercard Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MA stock on TIKR for Free →

You May Also Like

Justice Department has 'gone off the rails' for Trump's 'pretzel logic': analysis

Securitize Tokenizes $295M of Its Own Stock on Solana and Avalanche After NYSE Debut