Pepsi Price Prediction: The Case for 20%+ Upside

The post Pepsi Price Prediction: The Case for 20%+ Upside appeared first on 24/7 Wall St..

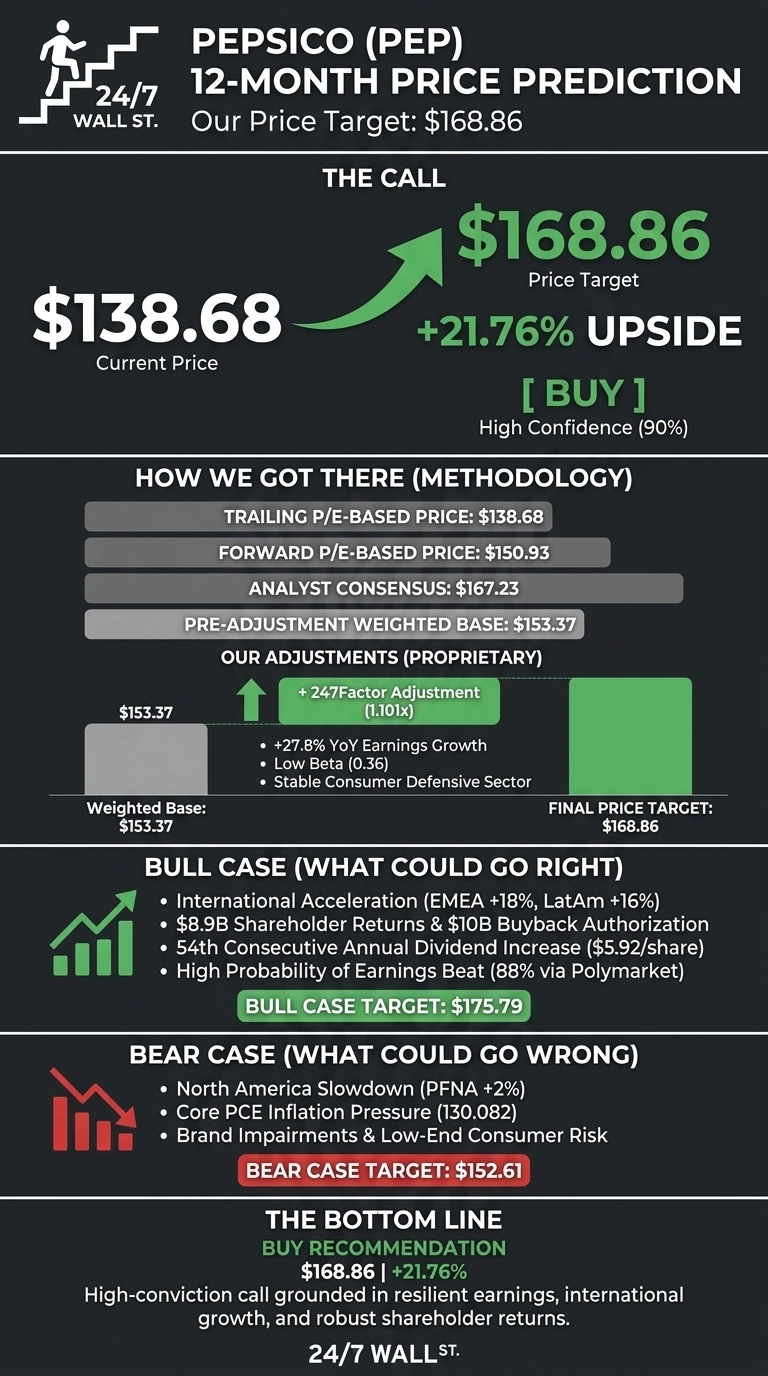

Our PepsiCo (NASDAQ:PEP) thesis starts with a number: the 24/7 Wall St. price target for Pepsi is $168.86, against a current price of $138.68. That implies 21.76% upside over the next twelve months.

Our recommendation is buy, with a model confidence level of 90%. In plain language, this is a high-conviction call grounded in resilient earnings, an undemanding forward multiple, and a dividend aristocrat profile trading well below its 52-week high.

24/7 Wall St.

24/7 Wall St.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $138.68 |

| 24/7 Wall St. Price Target | $168.86 |

| Upside | 21.76% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Pullback That Looks Like an Opportunity

Pepsi has slipped 2.82% over the past month and is down 1.49% year to date, even as the one-year return sits at a respectable 10%. Shares trade roughly 17% below the 52-week high of $168.19 and just above the 52-week low of $127.42.

The pullback comes despite a clean Q1 FY2026 earnings report: core EPS of $1.61 beat consensus by 4.26%, revenue of $19.443 billion beat by 2.75%, and operating margin expanded 210 basis points to 16.5%.

The international engine is humming. EMEA revenue grew 18%, Latin America Foods 16%, and Asia Pacific Foods 11%, with EMEA core operating profit up 29%.

The Case for $175+

The bull case rests on three pillars. First, the international business is accelerating, with EMEA and LatAm Foods running double-digit growth.

Second, the new $10 billion buyback authorization through February 28, 2030, plus $8.9 billion in total fiscal 2026 shareholder returns, provides a hard floor under EPS.

Third, Pepsi just delivered its 54th consecutive annual dividend increase to $5.92 per share. Polymarket traders assign an 88% probability that Pepsi beats its upcoming quarterly print. Our bull case scenario points to $175.79, a 26.76% total return.

What Could Go Wrong

The bear case starts with North America. PFNA grew just 2% in Q1, and the affordability problem at the low-end consumer is real. JPMorgan’s 2026 outlook explicitly flags that traditional value sectors like consumer staples may continue to struggle due to a deteriorating low-end consumer. Core PCE inflation sits at 130.082, near a 12-month high, which constrains further price hikes.

FY2025 operating income fell 19.57% on $1.86 billion of Rockstar and Be & Cheery impairments, a reminder that brand integration can disappoint. Bulls would counter that those were non-cash charges and core EPS still landed at $8.14. Our bear case scenario lands at $152.61, still a 10.04% return.

Pepsi Price Prediction 2026-2030

I am a buyer at $138.68. The 24/7 Wall St. price target of $168.86 reflects a 90% confidence buy, anchored by a 16x forward P/E, a 4.08% dividend yield, and accelerating international growth.

I would step up aggressively if North America volume turns positive next quarter. I would stay on the sidelines if EMEA growth decelerates below 10% or core EPS guidance is cut. With even the bear case projecting double-digit returns, the risk-reward favors buyers.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $168.86 |

| 2027 | $186 |

| 2028 | $205 |

| 2029 | $226 |

| 2030 | $251.13 |

These projections assume Pepsi continues delivering 5% to 7% core EPS growth and maintains its dividend growth streak. Material upside could come from a faster North America volume recovery; material downside could come from a sharper tariff-driven commodity shock.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and PepsiCo didn’t make the cut. Grab the names FREE today.

The post Pepsi Price Prediction: The Case for 20%+ Upside appeared first on 24/7 Wall St..

You May Also Like

3 Reasons Investors Are Following Mutuum Finance (MUTM) Since Q1 2025

Ethereum Institutional launched to boost Wall Street adoption after foundation layoffs